If you accept card payments in Australia, you are paying for them on one of two pricing models: flat rate, also called blended, or interchange-plus, often written as IC++. Flat rate gives you one simple percentage on every sale. Interchange-plus breaks the fee into its real parts and adds a fixed margin on top. The model you are on can change your bill by hundreds of dollars a month for the same turnover, and most small businesses are never told which one they have.

This guide explains both models in plain English, shows the maths with worked examples, and helps you work out which one is cheaper for your business. The short version is in the FAQ at the end, but the right answer depends on your volume and your card mix more than on any headline rate.

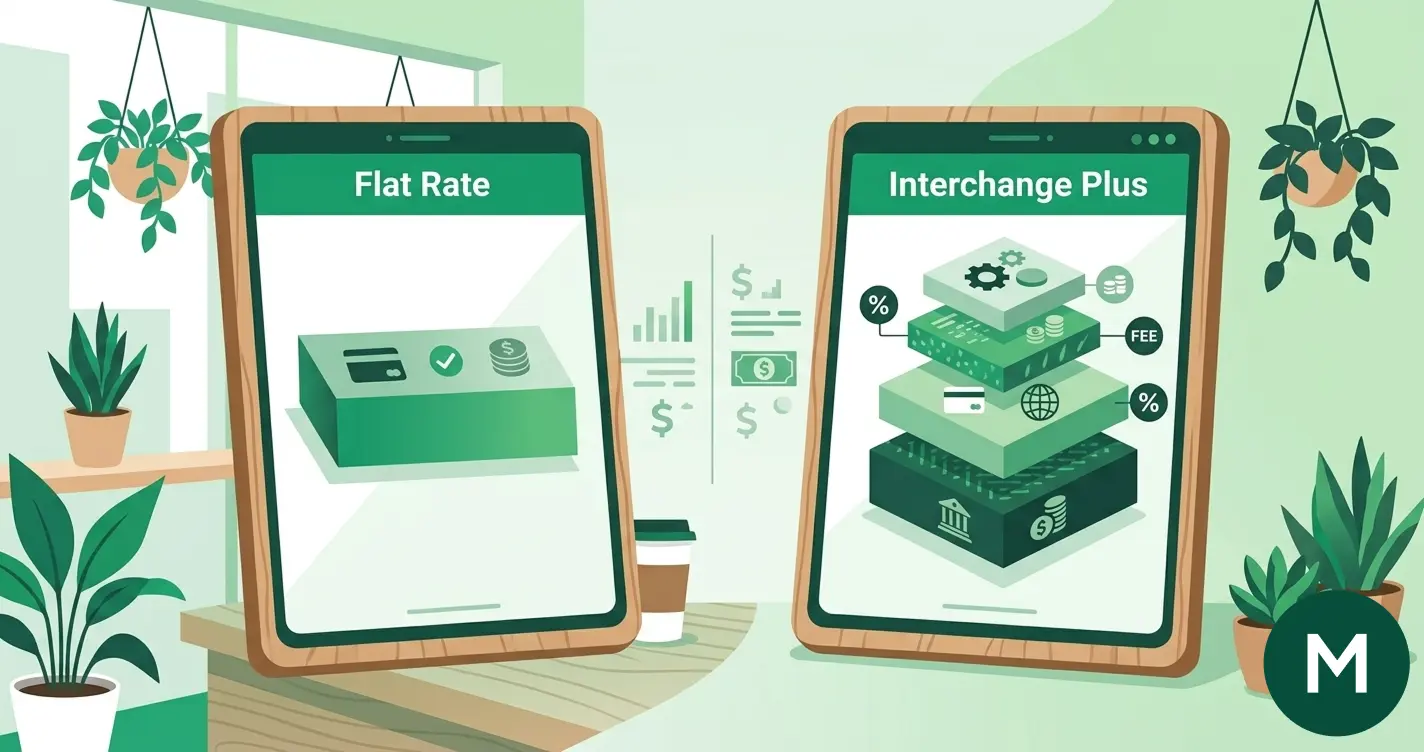

Flat-rate (blended) pricing, explained

Flat-rate pricing charges you a single percentage on every transaction, regardless of the card type. A tap from a basic debit card and a tap from a premium rewards credit card cost you exactly the same. The provider has blended all the underlying costs, the interchange fee, the scheme fee and their own margin, into one headline rate, which is why it is also called blended pricing.

The appeal is simplicity. You know your rate, you can predict your bill, and you never have to read a complex statement. Flat-rate plans are the default for most modern fintech providers, including Square, Zeller, SumUp and Stripe, and for flat-rate bank products such as CommBank Smart. You can see each provider's current published rate on our payment providers comparison.

The trade-off is that you are paying an average. On a cheap debit transaction that genuinely costs the provider very little, you still pay the full flat rate, so the provider keeps the difference. On an expensive premium card, the same flat rate may actually be a bargain. Across a typical card mix it evens out, but if your mix leans heavily towards low-cost debit, you are very likely overpaying on flat rate.

Interchange-plus (IC++) pricing, explained

Interchange-plus does the opposite: it shows you the real cost of each transaction and adds a transparent, fixed margin. Every card fee is built from three parts.

The four players

- 01IssuerCustomer's bank

Issues the Visa, Mastercard, or EFTPOS card.

Earns: Interchange

- 02SchemeCard network

Visa, Mastercard, or EFTPOS, the rails the message runs on.

Earns: Scheme fee

- 03AcquirerPayments provider (PSP)

Zeller, Square, Tyro, Stripe, CommBank, NAB, Westpac, or another.

Earns: Acquirer margin

- 04MerchantYou

Receive the payment minus the fees above.

Earns: The remainder

The five-step round trip

- 01Customer taps card

- 02Acquirer requests authorisation

- 03Scheme routes to issuer

- 04Issuer approves and replies

- 05Settlement lands next business day

- Interchange is set by the card schemes and paid to the customer's bank. It is the largest and most variable component, and it depends on the card type: debit is cheap, standard credit is more, and premium or commercial cards are the most expensive.

- Scheme fees are small charges paid to Visa, Mastercard or eftpos for running the network.

- The acquirer margin is what your provider keeps. In an interchange-plus deal this is the only negotiable part, and it is the same fixed number on every transaction.

Because interchange and scheme fees are simply passed through at cost, an IC++ rate is usually written as something like "interchange + 0.3%". That 0.3% is the margin; everything else is the true wholesale cost. Interchange-plus is the traditional model for the big banks and for high-volume specialists like Tyro and Adyen. It rewards businesses that take a lot of low-cost debit, because you pay the real low cost rather than a blended average.

How to tell which model you are on

The quickest test is your statement. If every transaction is charged the same percentage no matter the card, you are on flat rate. If you see a list of different rates by card type, or a line that reads as interchange plus a margin, you are on interchange-plus. A single headline rate in your sign-up paperwork, with no mention of interchange, almost always means blended pricing. If you cannot tell, ask your provider directly which model your plan uses and what the margin is. A provider that cannot answer that plainly is a flag in itself.

The maths: worked examples

The figures below are illustrative, to show how the two models behave on the same sale. Your actual rates depend on your provider and your negotiated margin, which you can check against live rates in our comparison.

| Example transaction | Flat rate (typical) | Interchange-plus (illustrative) |

|---|---|---|

| Debit card tap | around 1.4% to 1.6% | interchange ~0.1% + scheme ~0.05% + margin ~0.3% = about 0.45% |

| Standard credit card | around 1.5% to 1.7% | interchange ~0.3% + scheme ~0.1% + margin ~0.3% = about 0.7% |

| Premium rewards card | the same flat rate | higher interchange, so the total rises above the credit example |

The pattern is the giveaway. On debit, interchange-plus can be roughly a third of the flat rate, because debit interchange is tiny and you only pay your fixed margin on top. On a premium card the position can flip, and flat rate can be the cheaper deal because its blended average is lower than the real cost. This is why your card mix decides the winner. A business that takes mostly contactless debit saves the most on interchange-plus; a business whose customers mostly pay with rewards cards may do better on a flat rate.

It also explains a common surprise. Two businesses with identical turnover and identical headline rates can pay very different effective rates once you account for their card mix and pricing model. The effective rate, what you actually pay as a percentage of turnover once everything is counted, is the only number worth comparing.

When flat rate is cheaper

Flat rate tends to win for:

- Lower-volume businesses. Under roughly $20,000 a month in card turnover, the savings from interchange-plus are usually too small to outweigh its complexity, and many IC++ plans carry minimums or monthly fees that erode the benefit.

- A credit-heavy or premium-card mix. If most of your customers pay with rewards or premium cards, the blended average can be lower than paying real interchange on each one.

- Businesses that value simplicity. One rate, a predictable bill and no statement to decode has real value, especially for owner-operators without a finance team.

For most cafes, sole traders and small retailers, a competitive flat rate is the simplest good choice. Our guide to comparing payment providers walks through how to shortlist one for your business.

When interchange-plus is cheaper

Interchange-plus tends to win for:

- Higher-volume businesses. Once you are processing tens of thousands of dollars a month, shaving the margin and paying true interchange on debit adds up quickly.

- A debit-heavy mix. Hospitality, supermarkets and everyday retail take a lot of contactless debit, which is exactly where interchange-plus is cheapest.

- Businesses willing to read a statement. IC++ statements are more detailed, and you do need to check the margin is being applied as agreed. If you are happy to do that, the transparency pays off.

Interchange-plus also pairs well with least cost routing, which sends contactless debit down the cheaper eftpos network and compounds the saving on a debit-heavy mix. We cover how that works in the merchant fees guide.

Which providers use which model

| Pricing model | Typically offered by | Best suited to |

|---|---|---|

| Flat rate (blended) | Square, Zeller, SumUp, Stripe, plus flat-rate bank products | Small and medium businesses wanting simplicity and predictable costs |

| Interchange-plus (IC++) | Tyro, Adyen, and the big banks | Higher-volume or debit-heavy businesses willing to read statements |

Some providers offer both, or a flat headline rate with an interchange-plus option once you pass a volume threshold, so it is always worth asking. Current rates for every provider sit on our payment providers comparison, and you can model your own cost with the calculator there.

How the RBA reforms change the picture

The Reserve Bank's payments reforms reshape both models. Interchange caps lower the wholesale cost of cards, capping debit and consumer credit interchange, which flows straight through to interchange-plus merchants as a lower pass-through cost. Flat-rate merchants benefit too, but only if their provider chooses to lower its blended rate, so it is worth checking whether your rate has actually moved.

The bigger change is the surcharge ban from 1 October 2026, which stops merchants adding a surcharge on eftpos, Visa and Mastercard. Businesses that were passing fees to customers, including those on zero cost eftpos, will now absorb them, which makes the pricing model you are on, and the rate you pay, matter far more than when a surcharge hid the cost. We cover the detail in our RBA surcharge ban explainer and put the fee structure in context in the merchant fees guide.

How to negotiate an interchange-plus rate

If you are a candidate for interchange-plus, the margin is the only number you are really negotiating. A few things help:

- Know your numbers. Bring your monthly turnover, average transaction size and your debit-to-credit mix. High volume and a debit-heavy mix are your leverage.

- Negotiate the margin, not the interchange. Interchange and scheme fees are fixed costs that no provider controls. Push on the margin, and on any monthly or minimum fees attached to the plan.

- Ask about least cost routing. Make sure contactless debit is routed down the cheaper network by default, not the more expensive one.

- Get the full fee schedule in writing. Watch for terminal rental, PCI compliance fees, chargeback fees and lock-in terms that can quietly outweigh a good margin.

If you would rather not negotiate it yourself, our services team can review your statement, work out your real effective rate and benchmark it against the market.

The bottom line

Neither model is universally cheaper. Flat rate is the simpler, safer choice for lower-volume businesses and anyone with a premium-card-heavy mix, while interchange-plus rewards higher-volume, debit-heavy businesses that are willing to read a statement. The honest way to decide is to ignore the headline rate, work out your effective rate under each model for your real card mix, and compare. Our payment providers comparison and the annual merchant fees report are good places to start.

Frequently asked questions

What is the difference between interchange-plus and flat-rate pricing?

Flat-rate pricing charges one blended percentage on every card, regardless of type. Interchange-plus breaks the fee into its real parts, the interchange paid to the customer's bank plus scheme fees, and adds a fixed, transparent margin on top. Flat rate is simpler; interchange-plus is more transparent and often cheaper at volume.

Is interchange-plus always cheaper than flat rate?

No. Interchange-plus is usually cheaper for higher-volume or debit-heavy businesses, because you pay the true low cost of debit plus a small margin. Flat rate can be cheaper for lower-volume businesses or those with a premium-card-heavy mix, where the blended average works in your favour.

Which pricing model is better for a small business?

For most small businesses, a competitive flat rate is the better choice: it is simple, predictable and avoids monthly minimums. Interchange-plus becomes worth considering once your card turnover reaches the tens of thousands per month, especially with a debit-heavy customer base.

Do Square and Zeller use interchange-plus?

No. Square, Zeller, SumUp and Stripe all use flat-rate, or blended, pricing: one percentage on every transaction. Interchange-plus is more common with Tyro, Adyen and the big banks. You can compare each provider's model and current rate on our payment providers comparison. See how their flat rates stack up head to head in our Zeller vs Square comparison.

How do the RBA interchange caps affect my fees?

The Reserve Bank's interchange caps lower the wholesale cost of cards. Interchange-plus merchants see this immediately as a lower pass-through cost. Flat-rate merchants only benefit if their provider lowers its blended rate, so it is worth checking whether your rate has moved since the caps took effect.

How do I negotiate a better interchange-plus rate?

Focus on the margin, the only part a provider controls. Bring your turnover, average sale and debit-to-credit mix as leverage, push on monthly and minimum fees, and confirm least cost routing is switched on. Get the full fee schedule in writing before you sign. If you would rather not handle it yourself, our services team can review your statement and benchmark your rate against the market.