Every Australian business that accepts a card pays a merchant fee. It is the cost of moving money from your customer's bank into your settlement account, minus the cuts taken by the card network, the issuing bank, and your own payments provider. For most small businesses the effective rate sits between 1.1% and 2.5% of card turnover. That total is built from three components: interchange, scheme fees, and your provider's margin. This guide unpacks each one, shows you how to read your own monthly statement, and explains what changes when the RBA's new interchange caps take effect on 1 October 2026. Quick answers are in the FAQ at the bottom.

What are merchant fees?

A merchant fee is the price you pay your payments provider for accepting a card payment. On every Visa, Mastercard, EFTPOS, or AMEX transaction, a small percentage of the sale flows back through a chain of intermediaries before the rest lands in your account.

You pay these fees because someone has to compensate the players involved. Your customer's bank carries the credit risk and authorises the payment. The card network routes the message and polices fraud. Your provider supplies the terminal, the software, and the support line you ring when something breaks. Each one takes a share.

For an Australian small business, the effective rate (total fees divided by total card turnover) typically sits between 1.1% and 2.5%. The low end belongs to high-volume merchants on negotiated interchange-plus deals. The high end is what you pay when you sign up to a flat-rate online plan and never look at the statement again.

A worked example: on $50,000 a month in card sales, the gap between a 1.1% effective rate and a 2.0% effective rate is $5,400 a year. That is real money. The rest of this guide is about how to find it.

How a card transaction actually works

Behind every two-second card tap is a five-step process involving four players.

The four players

- 01IssuerCustomer's bank

Issues the Visa, Mastercard, or EFTPOS card.

Earns: Interchange

- 02SchemeCard network

Visa, Mastercard, or EFTPOS, the rails the message runs on.

Earns: Scheme fee

- 03AcquirerPayments provider (PSP)

Zeller, Square, Tyro, Stripe, CommBank, NAB, Westpac, or another.

Earns: Acquirer margin

- 04MerchantYou

Receive the payment minus the fees above.

Earns: The remainder

The five-step round trip

- 01Customer taps card

- 02Acquirer requests authorisation

- 03Scheme routes to issuer

- 04Issuer approves and replies

- 05Settlement lands next business day

Each step costs money. The issuer earns interchange. The scheme charges a small fee. Your provider keeps the margin that is left. The total is the merchant fee on your statement. Settlement runs overnight: the schemes net out balances between issuers and acquirers, and the cleared funds land in your settlement account the next business day (or the same day, if your provider offers it).

The three components of every merchant fee

Whichever provider you use, every merchant fee has the same three building blocks.

Interchange fee (paid to the issuer)

The biggest component, usually 50% to 70% of total cost. Your acquirer pays it to the customer's bank to compensate them for credit risk, fraud handling, and the rewards programs they fund.

Interchange rates are set by Visa and Mastercard but capped by the RBA. Under the May 2026 reform package, the cap on consumer credit interchange drops to 0.3% and the cap on debit interchange holds at 0.2%, both effective 1 October 2026. Full context on those reforms is in our RBA surcharge ban explainer.

Scheme fees (paid to Visa, Mastercard, or EFTPOS)

Small but real, typically 0.05% to 0.15% of transaction value plus a handful of fixed cents per tap. They pay for routing, fraud-monitoring tools, cross-border processing, and brand licensing. On flat-rate plans they are baked into the headline rate. On interchange-plus statements they appear as separate lines. Neither model gives you room to negotiate them.

Acquirer margin (paid to your provider)

What is left after interchange and scheme fees come out. This slice pays for terminal hardware, software, fraud risk, support, and the provider's profit.

It is the only component you can negotiate. Mid-size hospitality and multi-location retail above $50,000 a month should not be paying retail margin without a conversation. Providers like Tyro (Tyro provider page) and Stripe (Stripe provider page) will move on margin to win volume.

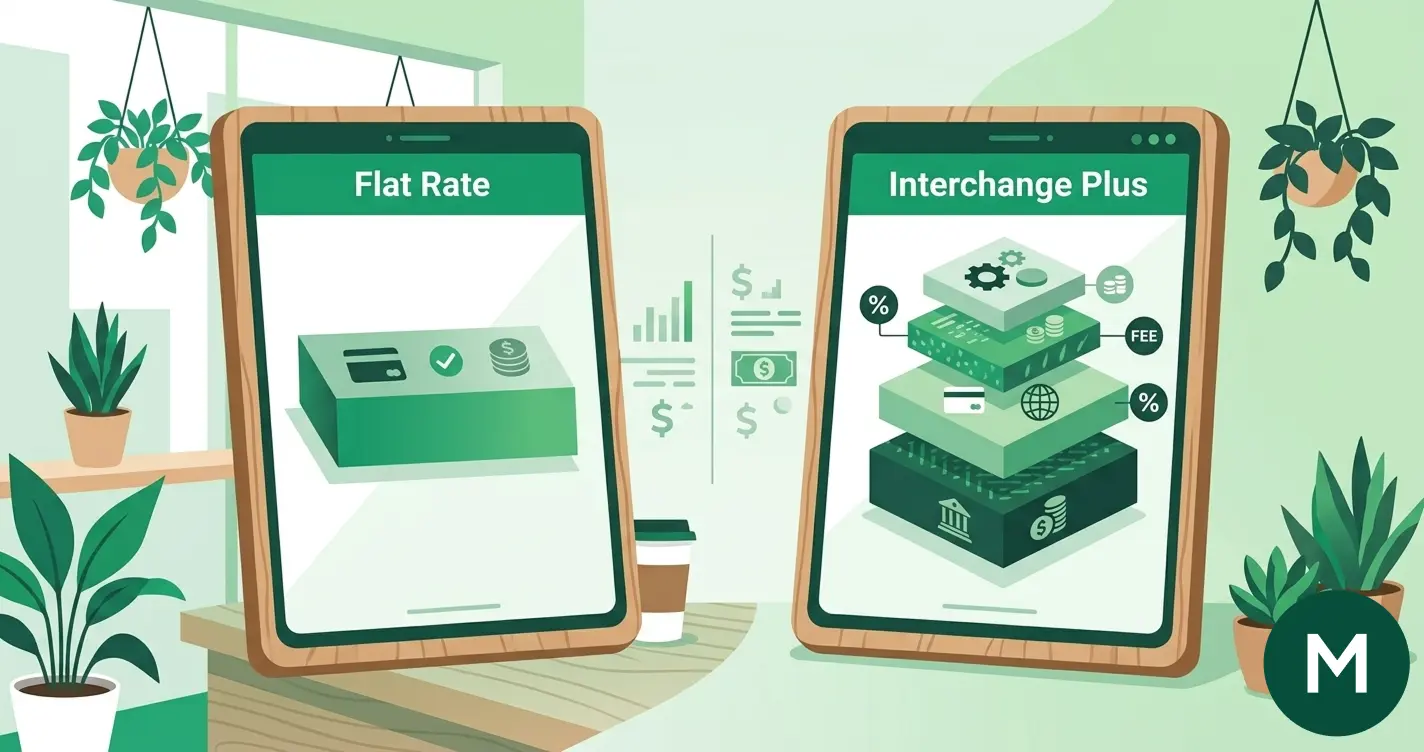

Blended pricing vs interchange-plus, explained simply

Australian providers offer two main pricing models. The difference matters more than most merchants realise.

Blended (flat-rate) pricing

You pay one headline rate on every transaction, regardless of card type. Zeller charges 1.4% inclusive of GST. Square charges 1.6%. CommBank Smart charges 1.1%. Whether the customer pays with a debit card costing the provider 0.2% in interchange or a premium credit card costing 1.5%, you pay the same.

You get predictability. Statements are short. Budgeting is easy.

You give up transparency. The provider keeps any saving when interchange drops, unless competitive pressure forces a cut. Flat-rate suits small to medium businesses under $1 million a year in card turnover, particularly in hospitality and small retail. See Zeller and Square for typical examples.

Interchange-plus pricing

You pay actual interchange, plus actual scheme fees, plus a fixed margin. A typical quote looks like "interchange + 0.30% + $0.10 per transaction".

Statements run to multiple pages, and the figures move every month with your card mix. The advantage is that on debit-heavy mixes the all-in cost can sit well below 1%. When the RBA caps take effect in October, the saving flows straight through. Best for venues above $1 million a year, anywhere with steady debit volume, and any operator who wants to see exactly where money goes.

A worked example: a $50,000-a-month merchant with a 70/30 debit/credit split pays roughly $800 a month on a 1.6% blended rate. The same merchant on interchange + 0.30% with average interchange of 0.25% pays closer to $275 a month. Compare live rates at our payment provider comparison.

How to read a merchant statement

Most merchants glance at the total at the bottom of their statement and file it. That is usually enough money left on the table every month to fund a second coffee machine. Seven lines to check on every statement:

- Total card turnover. Gross card transactions for the month. Should match your point-of-sale daily takings.

- Total fees. The absolute dollar amount the provider has taken. Compare this number across providers, not the headline rate.

- Effective rate. Total fees divided by total card turnover. If the statement does not show it, calculate it yourself. The single most useful number on the page.

- Per-transaction fees. Flat amounts (often $0.10 to $0.30) on each tap. They hit small-ticket merchants hardest. A cafe selling $5 coffees on a 1.4% plus $0.25 plan is paying an effective rate over 6%.

- Monthly platform or terminal fees. Fixed costs that show up whether you trade or not. NAB and Westpac charge around $25 a month rental. Zeller, Square, SumUp, and most CommBank plans do not.

- Chargeback fees. Per-dispute charges, usually $15 to $25, win or lose.

- PCI compliance fees. Either monthly or annual, often $10 a month or $99 a year. Sometimes hidden under different labels.

One common pitfall: providers that lead with "0% on debit" or "free EFTPOS" headlines usually recoup costs in higher credit rates, terminal rentals, or surcharge passes that become illegal on 1 October 2026. Read the whole statement, not the marketing. If a statement looks complicated, our services team does one-on-one reviews.

The hidden fees most merchants miss

Five fees that quietly add to your effective rate, in order of how often they catch people out.

Minimum monthly fees. Some providers, particularly Tyro and the big four banks, set a minimum spend (usually $20 to $30) that you pay even if you trade nothing that month. Quiet weeks in January or July cost more than they should.

Terminal rental. Free with Zeller, Square, and SumUp on entry plans (you buy the hardware once and own it). NAB charges $25 a month, Westpac $24.75. Over five years a rental adds up to several times the cost of the hardware.

Chargeback fees. Every time a customer disputes a transaction, you pay $15 to $25, win or lose. Online merchants in electronics, ticketing, or anywhere with high friendly-fraud should price chargebacks into their margin.

PCI compliance fees. Required if your business stores or transmits card data. Typically $99 to $300 a year. Most modern providers waive this if you use their hosted checkout, because the data never touches your servers.

International or cross-border fees. Foreign-issued cards usually cost an extra 1.0% to 1.5% on top of the headline rate. Matters if you serve tourists or run an online store with overseas customers.

A useful benchmark: a clean small-business plan in Australia should carry zero monthly fees, no PCI fee on a hosted checkout, and a chargeback fee under $25. If your statement has more line items than that, you are paying for things you can probably remove.

Australian provider rates compared (May 2026)

The Australian market has roughly ten providers competing for small and mid-sized merchant business. Headline rates as of May 2026:

| Provider | In-person | Online | Monthly | Pricing model |

|---|---|---|---|---|

| Zeller | 1.4% (incl. GST) | 1.7% + $0.25 | $0 | Flat-rate |

| Square | 1.6% | 2.2% | $0 | Flat-rate |

| CommBank Smart | 1.1% | quote | $0 | Flat-rate |

| SumUp | 1.4% | quote | $0 | Flat-rate |

| Tyro | quote | 1.7% + $0.30 | quote | Interchange-plus |

| Stripe | 1.7% + $0.30 | 1.7% + $0.30 | $0 | Flat or interchange-plus |

| NAB | 1.15% / 1.4% Easy Tap | quote | $25 rental | Flat-rate |

| Westpac | 1.2% / 1.4% Air | quote | $24.75 rental | Flat-rate |

Rates current at May 2026. The right provider depends on card mix, turnover, and hardware preferences. Run a live fee calculation at our payment provider comparison.

The RBA's new interchange caps

On 31 March 2026, the RBA announced new caps on interchange fees that take effect on 1 October 2026.

The package has three moving parts. The cap on interchange for domestic consumer credit cards drops to 0.3%. The cap on debit interchange holds at 0.2% under the same review. Surcharging on EFTPOS, Visa, and Mastercard transactions is banned from the same date.

What this means for your fees depends on your pricing model. If you are on interchange-plus, the saving on consumer credit appears automatically on your October statement. Most mid-size venues will see their effective rate drop by 0.1% to 0.2% depending on debit/credit mix.

If you are on flat-rate pricing, the cap does not move your rate on its own. The provider keeps the saving as margin unless the market forces a cut. Watch competitor pricing through Q4 2026 and the start of 2027, and be ready to renegotiate or switch.

The surcharge ban side of the same package is the bigger immediate change for hospitality and small retail. The full breakdown of who is affected and what to do sits in our RBA surcharge ban guide.

Frequently asked questions

What is a merchant fee?

A merchant fee is what a business pays its payments provider for accepting a card. It has three parts: an interchange fee paid to the customer's bank, a scheme fee paid to the card network, and the provider's margin. For most Australian small businesses, total fees sit between 1.1% and 2.5% of card turnover.

What is a good merchant fee rate in Australia?

A competitive in-person rate sits between 1.1% and 1.6% on flat-rate plans in 2026, with leaders like CommBank Smart at 1.1% and Zeller at 1.4%. Online rates run higher, typically 1.7% to 2.2%. Above $1 million a year in turnover, interchange-plus deals can push effective rates well below 1% on debit-heavy mixes.

Are merchant fees tax deductible in Australia?

Yes. Merchant fees are a fully deductible business expense in the period they are incurred. They reduce your assessable income line by line on the statement. Treat them like any other operating cost, and speak to your accountant about how to record them in your accounting software and which BAS lines they affect.

What is the difference between interchange and the merchant fee?

Interchange is one component of the merchant fee, not the whole thing. Interchange is the wholesale fee your acquirer pays to the customer's bank on every transaction. The merchant fee is the all-in retail rate you pay your provider, which includes interchange, scheme fees, and the provider's margin combined.

Can I negotiate my merchant fees?

Yes, particularly on the margin component. Above $30,000 a month in card turnover, most providers will discount margin to keep your business. Above $100,000 a month, an interchange-plus deal is usually on the table. Bring three months of statements and a competitor quote to the conversation. Per-transaction fees are also negotiable.

What is changing in October 2026?

Two things. First, surcharging on EFTPOS, Visa, and Mastercard becomes illegal from 1 October 2026. Second, the cap on interchange for consumer credit cards drops to 0.3%, and debit interchange holds at 0.2%. Together the RBA estimates the package will reduce merchant fees by $910 million a year. Full detail is in our RBA surcharge ban guide.

The bottom line

Merchant fees have three components, two pricing models, and a half-dozen line items worth checking on every statement. The cheapest provider is not always the lowest headline rate. It is the plan whose pricing model fits your card mix and turnover. The second half of 2026 is the most competitive window in a decade because of the RBA changes. Compare ten Australian providers on live rates in under five minutes, or talk to our services team for a one-on-one statement review.